Per-token costs are collapsing. Total AI coding spend is climbing anyway. That isn’t a contradiction. It’s a 160-year-old paradox doing exactly what it has always doing.

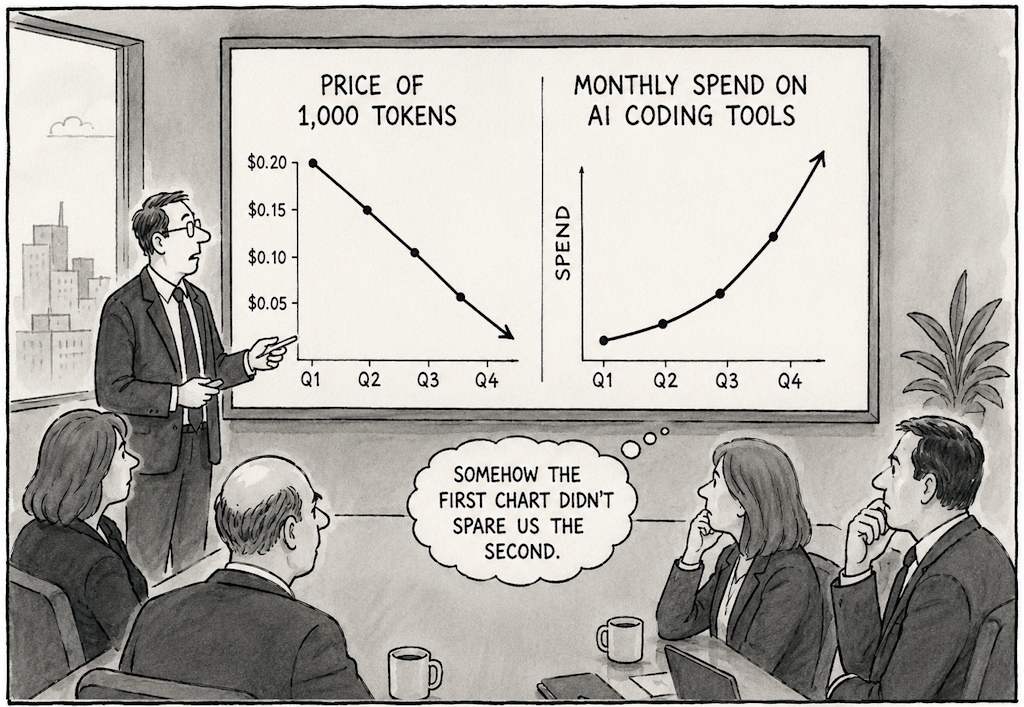

Somewhere in second quarter there will be a budget review where two slides will appear to be in disagreement. One shows the price of a thousand tokens, and the line slopes down and to the right, the way the cost of a maturing technology is supposed to. The next slide shows the monthly spend on AI coding tools, and that line climbs up and to the right, steeply, and nobody in the room can quite say why the first chart didn’t spare them the second. Jevons’ Paradox settles this disagreement.

By 2028, Gartner predicts, the cost of AI coding will overtake the salary of the average developer. Sit with that, because the number is doing a lot of work: the tools sold to us as a way to make engineers cheaper are on course to cost more than the engineers. Juxtaposed this against this forecast Gartner stated just three months earlier where they stated the cost of running these models is projected to fall by more than 90% by 2030. These two predictions by Gartner at a glance do look incompatible. They are not. They are not even in tension. The fact that reconciles them is old enough to have been named in 1865. What I want to flag first is that the apparent paradox is a misdirection. “Why is the bill rising?” turns out to be the easy question, and it has a boring answer. The question worth your attention is the one underneath it, quieter and far less comfortable: is the rising bill buying anything? And the very thing everyone reaches for to explain the bill is, by its nature, silent on precisely that.

Whether “the average developer’s salary” is even the right yardstick is a separate problem. A fixed, budgeted number propped up next to a variable, metered one, as if the two were the same kind of thing and I take that up elsewhere. Here I’ll grant Gartner the comparison and look at what sits beneath it.

Tokens are coal

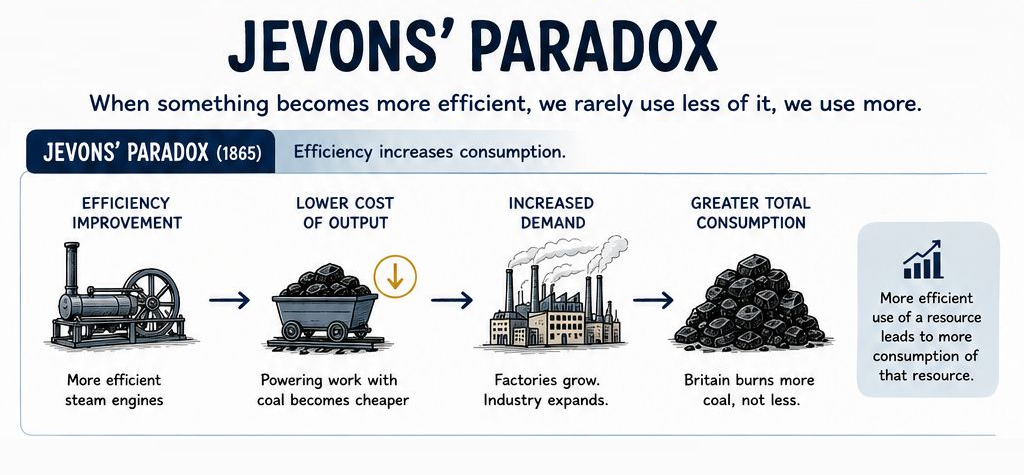

It is a confusion of ideas to suppose that the economical use of fuel is equivalent to a diminished consumption. The very contrary is the truth — W.S. Jevons, The Coal Question, 1865

In 1865 the economist William Stanley Jevons noticed something about coal that nobody wanted to hear. Steam engines were getting more efficient (more work wrung from every lump) and the logical expectation was that England would therefore burn less of the stuff. The opposite happened. Cheaper, more efficient steam made steam worth using for things it had never been worth using for before, and national coal consumption went up. Efficiency did not curb demand. It created demand. That counterintuitive result has carried his name ever since: the Jevons paradox.

In AI world, tokens are coal. As the cost of a unit of machine work falls, we do not bank the savings and walk away. We go looking for more things to point the machine at. The casual user who pasted in a single function last quarter is running an agent across the entire repository this quarter. Gartner expects exactly this, the occasional dabbler hardening into a daily user as the habit takes hold. The agent that used to answer one question now runs in a loop until it’s satisfied. The autonomy ladder gets climbed rung by rung, and each new rung feels cheaper at the moment, because per-token it genuinely is. Now multiply “cheaper at the moment” by a surging count of moments. You get a bill that swells even as every token on it gets cheaper. The down-and-to-the-right slide and the up-and-to-the-right slide were never arguing. They were describing two sides of the same coin.

I should name the assumption holding this up rather than slip it past you. The whole story depends on demand being elastic. Elastic enough that consumption outruns the falling price. If it isn’t, if teams reach some natural ceiling on how much AI work they actually want done, the effect stalls and the bill flattens of its own accord. That is a real possibility.

Not all of the rising bill is Jevons. Some of the increase is the industry quietly unwinding its subsidies and migrating from flat seat licenses to metered pricing. A shift that can push the price you pay up even while the cost of producing a token falls, as infrastructure build-out and the long-deferred demand for profit start working their way into list prices.

Price, Spend, and Value

Here is the sleight of hand the coal analogy performs, and the one move you must not let it make for free. When we tell the Jevons story about coal, we quietly assume the extra coal went into productive engines: that the new consumption did real work and earned it. Jevons connects a falling price to a rising spend. He says nothing, on his own, about value. With coal we supply the value silently. With tokens we do not get that luxury, and we should stop pretending we do.

Price → Spend → Value

Jevons spans the first arrow and is blind to the second. It explains why cheaper tokens produce a bigger bill. It has nothing whatsoever to say about whether the bigger bill bought you anything.

And you cannot read the answer off your usage dashboard, however granular it is. Maybe the marginal token, the one you only bought because it was cheap, went to reformatting a file that was fine to begin with, and the value it returned rounds to zero. Or maybe that same token funded work that was never economical at the old price: the exhaustive test suite no one would have hand-written, the gnarly refactor no one would have signed off on when it cost a senior engineer a week. Both of those stories produce the identical invoice. Tokens consumed cannot distinguish between them, because tokens consumed is a measure of activity, and the thing you actually care about is outcome/value.

I’ve made an adjacent argument before. Tokens consumption makes a terrible target: promote that number to a goal and a person will cheerfully manufacture it for you, value be damned. That’s a story about gaming the system I’ve told before. This is a different and subtler story, the one that survives whether the gaming has been stamped out or not. Even when every token is spent in perfect good faith, by engineers with no leaderboard to climb and nothing to prove, the count still cannot tell you whether the spend created value. The blindness isn’t a behavioral failure. It’s structural. Likewise, just because a steam engine is more efficient does not mean every train is headed to its destination with full passengers. Output/value of that train is low, maybe negative.

The only instrument that could see value measures something brutal and inconvenient: the output of an engineer working with the AI, minus the output of that same engineer working without it, weighed against the cost of the tokens that made the difference. That gap is the value. It also demands a speculation: the same person, the same task, the road not taken. This is very nearly impossible to measure cleanly in the wild. That difficulty is the whole reason the question stays open. It is not that no one has bothered to look. It is that the one number worth having is the one number that refuses to be counted.

Whether the spend is, on balance, justified is a real question and a fair one. I am deliberately not answering it here. That’s a different essay, and answering it in passing would be exactly the kind of overreach this one is arguing against.

So what?

If you want a metrics worth tracking rather than a number worth panicking over, you first have to pull apart two claims I’ve been carrying together, because they fail in completely different ways.

The first is descriptive: rising spend is consistent with falling cost. This is true, and it is also nearly unfalsifiable. Almost any spending pattern is “consistent with” almost anything, which is precisely why being right about it earns you nothing. It’s the correct frame. It is not where the risk lives, and I don’t want to be congratulated for a claim that can’t lose. The risk lives in two other claims, and these can both be wrong. (1) That the demand is elastic enough for the Jevons response to dominate rather than quietly saturate. (2) That the value gap is real and, as of today, unmeasured. Here is how you’d catch either one out.

For the value gap, Déjà Vu already handed us the instrument: look at the real workflows and count how many of them still have a human doing substantial review, correction, and judgment downstream of the model. If that headcount is falling while the work ships, the marginal token is doing real work and the gap is closing. If it’s holding steady or worse rising while spend climbs, then you are paying to generate output that a human then has to redo, and the gap is not merely real, it is widening on your dime.

For whether this is a transformation that sticks or one that shrinks back to its actual, more modest size: a transformation in retreat reveals itself through persistent high unit cost to maintain quality. By that measure, a per-token cost that keeps falling is the signature of a sticky transformation, not a failing one. Which leaves a clean, stated set of conditions:

- The “sticky transformation” reading dies if per-token cost plateaus while spend keeps climbing.

- The elasticity bet dies if usage saturates as the price falls. If the bill flattens without anyone forcing it to.

- The value question stays open until someone measures that counterfactual honestly. I’d meet anyone who claims to have closed it with a raised eyebrow and a request to see the control group.

What’s left?

It would be easy, and wrong, to read all of this as reassurance. It’s only Jevons, it’s only economics, the model keeps getting cheaper, go back to sleep. That is the single conclusion I’d steer you away from. Jevons is not the comfort in this story. Jevons is the diagnosis of why the pain is real. The falling price is the very thing driving the bill up, which means “but the model got cheaper” is cold comfort indeed to the team that torched its quarterly budget somewhere around the second month. Efficiency here is the cause, not the cure, and treating the cure as if it were also the remedy is how you end up surprised by your own invoice.

And then there is the sharper discomfort, the one left sitting on the table after the budget is reconciled: the same reasoning that explains your bill in full cannot certify that the bill was worth paying. That’s not a rough edge in the current tooling that a better dashboard will sand down next year. It’s structural. The value term is hard to measure for the same reason it’s the only term that matters. Because it’s the one tied to whether real work got done.

Which is exactly why the disciplined responses: engineering the context you feed the model instead of dumping the world into it, routing the easy, high-volume work to smaller models and reserving the expensive ones for problems that earn them, governing how much autonomy an agent is actually handed. These are not a matter of waiting for prices to fall. Prices falling is what created the problem. The work is to govern the elasticity, and to narrow, not close. I don’t believe you can close it. The gap between what you spend and what you can point to and call a result. So watch two curves, and don’t confuse them. The first is whether the unit cost keeps falling, and you’ll have that answer soon enough; everyone is already charting it. The second is whether anyone, anywhere, can demonstrate that the marginal token earned its value. The first curve is the one the whole industry is watching. The second is the one that actually decides this. And as of today, nobody has drawn it.